Due Diligence

Understanding the SECURE Act’s Impact on IRAs Left to Trusts

In 2019, the SECURE Act introduced significant changes to retirement accounts, and in 2022, the IRS provided proposed regulations that surprised many financial professionals. Now, in 2024, the IRS has finalized these rules, and they have a big impact on how IRAs left to trusts are managed. These regulations clarify some aspects but also introduce complexity, which could lead to potential tax issues.

Why Leave an IRA to a Trust?

People often name a trust as the beneficiary of an IRA to:

- Protect assets from creditors (especially after the 2014 Supreme Court decision in Clark v. Rameker, which removed some creditor protections for inherited IRAs).

- Control how funds are distributed to beneficiaries, especially if they are minors or have spending issues.

- Provide financial support for special needs beneficiaries while preserving government benefits.

Before the SECURE Act, trusts could “stretch” IRA distributions over the life expectancy of the beneficiary, helping to minimize tax burdens. Now, however, the rules have changed significantly.

Key Steps in Determining Trust Distribution Rules

The final regulations introduce a multi-step process for determining how an IRA left to a trust will be distributed:

Step 1: Is the Trust a “See-Through Trust”?

A see-through trust allows the IRS to recognize the beneficiaries of the trust as the actual IRA beneficiaries. To qualify:

- The trust must be legally valid.

- It must be irrevocable upon the IRA owner’s death.

- The beneficiaries must be identifiable.

- The trustee must provide proper documentation to the IRA custodian.

If a trust does not meet these conditions, it is treated as a non-designated beneficiary, meaning the IRA must be liquidated within five years (if the owner died before their required beginning date) or follow the owner’s existing withdrawal schedule.

Sub-Trusts

If a trust splits into sub-trusts after the IRA owner’s death, each sub-trust is analyzed separately to determine distribution rules.

Step 2: Conduit vs. Discretionary Trusts

- Conduit Trusts: IRA withdrawals must immediately be paid out to the trust beneficiaries. Only the primary beneficiaries are considered when determining the payout period.

- Discretionary Trusts (also called accumulation trusts): IRA distributions can remain in the trust instead of being immediately distributed. However, all potential beneficiaries must be considered when determining payout rules.

Examples:

- A conduit trust with a spouse as the primary beneficiary can stretch distributions over the spouse’s life.

- A discretionary trust with multiple beneficiaries may be forced into a 10-year distribution period.

Step 3: Who Are the Trust’s Beneficiaries?

Beneficiaries fall into three categories:

- Eligible Designated Beneficiaries (EDBs) – These include surviving spouses, minor children (until age 21), disabled individuals, and those within 10 years of the original IRA owner’s age. They can still stretch distributions over their life expectancy.

- Non-Eligible Designated Beneficiaries (NEDBs) – Most adult children and other beneficiaries fall into this group. They must follow the 10-year rule, meaning the entire IRA must be withdrawn within 10 years.

- Non-Designated Beneficiaries – Estates, charities, and non-qualifying trusts fall into this category. These generally follow the 5-year or “at least as rapidly” rule.

Step 4: Determining the Distribution Options

The available distribution options depend on the beneficiary category and whether the IRA owner passed before or after their Required Beginning Date (RBD).

Scenarios:

- If the IRA owner passed before their RBD:

- EDBs can stretch distributions or choose a 10-year deferral.

- NEDBs must withdraw the full balance within 10 years.

- Non-designated beneficiaries must follow the 5-year rule.

- If the IRA owner passed after their RBD:

- EDBs can stretch payments, but they must take Required Minimum Distributions (RMDs).

- NEDBs still follow the 10-year rule but must take RMDs annually.

- Non-designated beneficiaries must take RMDs based on the deceased owner’s life expectancy.

Special Rule: Applicable Multi-Beneficiary Trusts (AMBTs)

A new category called AMBTs allows certain trusts benefiting disabled or chronically ill individuals to qualify for more favorable distribution options. These trusts are treated as conduit trusts, meaning the disabled beneficiary can stretch payments over their lifetime.

Planning Considerations

- If you want to preserve the stretch option, ensure the trust qualifies as a see-through trust and that all considered beneficiaries are EDBs.

- If a trust includes NEDBs, it will likely be subject to the 10-year distribution rule instead of a lifetime stretch.

- Consider Roth IRAs, as they are not subject to lifetime RMDs, which can provide more flexibility under the 10-year rule.

LPL Financial, Daniel Romero and their respective representatives do not provide tax, accounting, or legal advice. Any tax statements contained herein were not intended or written to be used and cannot be used for the purpose of avoiding U.S. federal, state, or local penalties. Tax laws are complicated and subject to change. Tax results may depend on each taxpayer’s individual set of facts and circumstances. Clients should rely on their own independent advisors as to any tax, accounting, or legal statements made herein.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.

Market Minute | March 04, 2025

Tune in to today’s #RWM #MareketMinute to hear the latest with #Trump #tariffs, market #volatility, and #portfolio impact. #stayinformed #educatedinvestor #wealthmanagement

Daniel Romero, Cfp® of Romero Wealth Mgmt. Recognized as One of Lpl Financial’s Top Financial Advisors

[Orange, CA] — [January 2025] – Daniel Romero, CFP® a financial advisor at Romero Wealth Management in Orange, today announced that his achievements have been recognized with inclusion in LPL Financial’s Masters Club Program* for 2025. This distinction celebrates a select group of advisors who have achieved excellence in financial guidance. It is more important than ever that Americans have an experienced financial partner by their side who understands their unique needs and can help them create and follow a plan for their future.

Romero serves clients based in Southern California, providing comprehensive wealth management services, including: investment management, retirement planning, tax planning, charitable giving, estate planning.

“On behalf of the entire team at LPL, I am thrilled to congratulate Daniel Romero on his outstanding achievements in 2024,” said Julian Lopez, LPL’s Executive Vice President of Independent Advisor Services Client Success. “Daniel has elevated his business across Southern California. His professional guidance has been crucial in empowering his clients to transform their financial dreams into tangible outcomes.”

Romero has been affiliated with LPL Financial, a leading wealth management firm, for 27 years. Through LPL, financial advisors are empowered to focus on their unique skills in building relationships and delivering personalized financial advice, while leaning on LPL to provide the services, support, and tools to help increase operational efficiency and power business growth.

About LPL Financial

LPL Financial Holdings Inc. (Nasdaq: LPLA) is among the fastest growing wealth management firms in the U.S. As a leader in the financial advisor-mediated marketplace, LPL supports more than 28,000 financial advisors and the wealth management practices of approximately 1,200 financial institutions, servicing and custodying approximately $1.7 trillion in brokerage and advisory assets on behalf of 6 million Americans. The firm provides a wide range of advisor affiliation models, investment solutions, fintech tools, and practice management services, ensuring that advisors and institutions have the flexibility to choose the business model, services, and technology resources they need to run thriving businesses. For further information about LPL, please visit www.lpl.com

Securities and advisory services offered through LPL Financial (LPL), a registered investment adviser and broker-dealer, member FINRA/SIPC.

LPL Financial and its affiliated companies provide financial services only from the United States.

Throughout this communication, the terms “financial advisors” and “advisors” are used to refer to registered representatives and/or investment adviser representatives affiliated with LPL Financial.

We routinely disclose information that may be important to shareholders in the “Investor Relations” or “Press Releases” section of our website.

*Achievement is based on annual production among LPL-affiliated investment programs only.

Market Minute | January 09, 2025

Happy New Year = Happy Market? Tune in for 2025’s first #RWM #MarketMinute where Dan talks #equity #portfolios, the #Fed, and #bonds.

Politics and Investing

It would be safe to say that this election season intensified emotions and left many investors uncertain of how the results could impact equity markets and their investments.

However, savvy investors have learned that equity markets have historically cared more about an election being over than they have about who won. While you may be disappointed that the person you voted for did not win, stock prices are nonpartisan. They are more commonly tied to earnings and corporations’ health than politics. What equity markets do not like is uncertainty, and the period prior to an election is filled with just that, especially during this most recent, particularly tense election campaign.

Company earnings, valuations, and the Federal Reserve have historically affected equity markets more than election results. Strong companies find ways to survive under both Democratic and Republican Presidents. For instance, companies like Apple will continue to develop and recreate their iPhones, and Amazon will continue to deliver packages regardless of who wins the election. The best-run companies typically find ways to advance, regardless of who occupies the White House.

History has proven that a well-balanced, diversified plan that eliminates emotion is in the best interest of any investor. The election results have left many either optimistic or pessimistic about the coming years. This can test the confidence of many investors, tempting them to make emotional moves in their financial plans.

Making investment decisions solely based on the election results is not recommended. Emotional investing, or trying to time the market, is typically challenging, if not impossible. Seasoned investors adjust their holdings based on the unique circumstances they are facing and the desired result they are looking to accomplish. A sound investment strategy should focus on the long-term instead of current events or short-term fluctuations.

As your financial professional, it is our responsibility to help you invest wisely to pursue your goals. If you are nervous or concerned about your situation, please call our office and schedule some time to speak with us.

Securities and advisory services are offered through LPL Financial, a registered investment advisor. Member FINRA/SIPC.

Note: The views stated in this letter are not necessarily the opinion of LPL Financial. This information is not intended to be a substitute for specific individualized tax, legal or investment planning advice as individual situations will vary. For specific advice about your situation, please consult with a lawyer, tax or financial professional. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. Stock market. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. Diversification is a method used to help manage investment risk; it does not guarantee a profit or protect against investment loss.

Sources: Yahoo Finance; Contents provided by the Academy of Preferred Financial Advisors, Inc.

Market Minute | 6, 2024

Post #presidential #election update: #Republicans sweep the #HouseofRepresentatives and the #Senate. The #market is reacting favorably at this news, but remember to think #longterm, especially about #taxbreaks, as #investing is about #goals. #stayinformed #educatedinvestor #wealthmanagement

Market Minute | Oct 25, 2024

Happy Friday! In today’s #RWM #marketminute, let’s talk #rivalry as #baseball #worldseries kicks off tonight, and as #technology #giants have a battle of the #marketshare. Stay tuned and #stayinformed. #educatedinvestor #wealthmanagement

Market Minute | Oct 04, 2024

Happy Friday! Join us for today’s #RWM #marketminute! Today we’re talking #jobs, union #strikes, and the #Fed. #stayinformed #educatedinvestor #wealthmanagement #cfp

Proactive Year-end Tax Planning for 2024 and Beyond

One of our main goals as holistic financial professionals is to help our clients recognize tax reduction opportunities within their investment portfolios and overall financial planning strategies. Staying current on the ever-changing tax environment is a key component to helping our clients benefit from potential tax reduction strategies.

Other than some IRS inflation adjustments, calendar year 2024 has brought limited changes in tax laws for individuals. This report focuses on information that could be helpful for individuals when tax planning for the calendar year 2024. Since 2025 is a presidential election year and both candidates have discussed tax rule modifications, it is highly likely that changes to both income tax and estate tax rules changes may be proposed. Also, please remember that the Tax Cuts and Jobs Act (TCJA) enacted in 2017 brought many changes to the tax code, including many provisions for individuals that are currently set to expire after 2025. Our goal with this report is to focus on current tax rules, understanding that one of the major uncertainties for all taxpayers is what will happen to the tax code in or after 2025.

As financial professionals, we try to be proactive. The primary objective of this report is to share strategies that could be effective if considered and implemented before year-end. Please note that this report is not a substitute for using a tax professional. In addition, many states do not follow the same rules and computations as the federal income tax rules. Make sure you check with your tax preparer to see what tax rates and rules apply to your state.

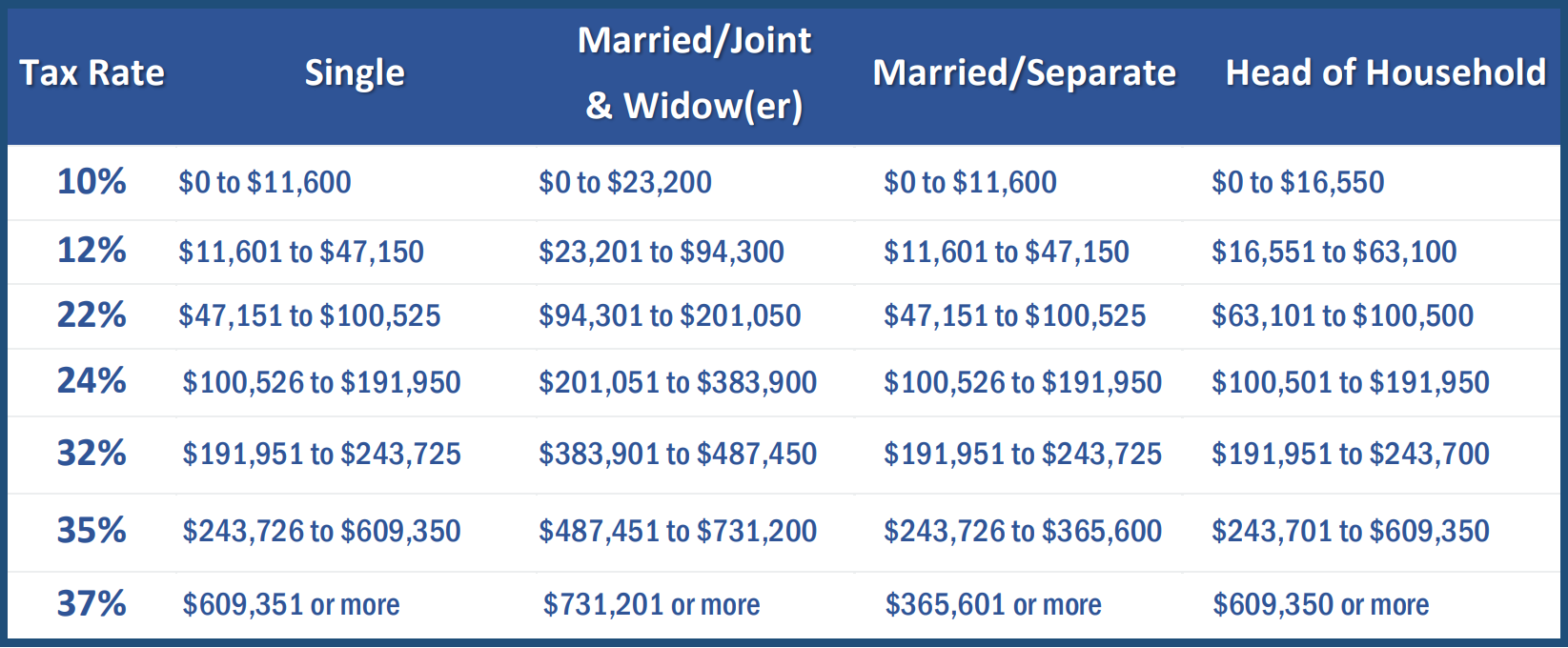

Income Tax Rates for 2024

For 2024, there are still seven tax rates. They are 10%, 12%, 22%, 24%, 32%, 35%, and 37%. Under current law, this seven-rate structure will be phased out on January 1, 2026.

Year-end Tax Planning for 2024

One of our foremost goals is to help our clients try to optimize their tax situations. This report offers many suggestions and reviews of strategies that can be useful to achieve this goal.

Everyone’s situation is unique, but it is wise for every taxpayer to begin their final year-end planning now! Choosing the appropriate tactics will depend on your income and several other personal circumstances. As you read through this report, it could be helpful to note those strategies that you feel may apply to your situation so you can discuss them with your tax preparer.

Click here to download a PDF of this report.

Market Minute | Sept 05, 2024

#RWM #marketminute #portfolio

Happy September! In this week’s #RWM #marketminute, Dan discusses #portfolio #changes, #longterm vs. #shortterm #investments, and potential #returns. #stayinformed #educatedinvestor #wealthmanagement ART#625607