Due Diligence

Romero Wealth Management, Inc. Embraces Fiduciary Excellence

Our firm was founded on the principles of integrity, professionalism and exceptional client service. We are also deeply committed to continuous improvement. Our dedication to doing what is best for you, our clients, prompted us to engage CEFEX, the Centre for Fiduciary Excellence, of Broadridge Fi360 Solutions, to audit our processes.

In May of 2025, we contacted the CEFEX organization and requested an independent analyst provide us with a comprehensive independent review. The process was rigorous and their assessment took months to complete. Now, after going through the audit and carefully evaluating our procedures, we are proud to share with you that Romero Wealth Management, Inc. is a CEFEX certified Investment Advisor.

This certification signifies our commitment to uphold the highest level of fiduciary care and that has a direct impact on you, your plan and your employees. As a plan sponsor, the Department of Labor (DOL) identifies the following as your fiduciary responsibilities:

- Act solely in the interest of plan participants and their beneficiaries and with the exclusive purpose of providing benefits to them;

- Act prudently in the faithful performance of all duties;

- Follow the plan documents (unless inconsistent with ERISA);

- Diversify plan investments; and

- Pay only reasonable plan expenses.

By working with Romero Wealth Management, Inc., you can rest assured that our actions align with these responsibilities; our prudent process aims to help you limit liability and build a retirement plan that strives to improve retirement outcomes.

CEFEX is an independent global assessment and certification organization. It works with industry experts to provide comprehensive assessment programs designed to improve the fiduciary practices of investment advisors, stewards (retirement plans, foundations and endowments, etc.), investment managers, and other financial service providers. CEFEX confers a formal certification for those firms that are willing to undergo an independent audit and able to demonstrate that they fully conform to high standards which are substantiated in case law and fiduciary best practices.

At Romero Wealth Management, Inc., we follow well-defined processes, grounded in best practices, so that we can make sound, objective, and consistent decisions in service to our clients. CEFEX certification offers testament to the fact that we understand the importance of paying close attention to everything from high level strategies and policies all the way down to the details of our business practices. The CEFEX Mark seeks to make our clients confident that we are worthy of their trust.

We wanted to share news of the important recognition of our commitment to fiduciary excellence and continuous improvement. CEFEX certification is yet another way we tangibly demonstrate that serving our clients’ best interests is our highest priority.

For more information about Romero Wealth Management, please contact us at [email protected] and (714) 547-8787.

About CEFEX®:

CEFEX®, Centre for Fiduciary Excellence, a division of Broadridge Fi360 Solutions, is an independent certification organization. CEFEX works closely with industry experts to provide comprehensive assessment programs to improve the fiduciary practices of investment stewards, advisors, recordkeepers, administrators and managers. Learn more at www.cefex.org.

CEFEX and Romero Wealth Management are separate, unaffiliated entities.

LPL Tracking #1-770763

Preferred Stocks vs. High Yield Bonds: Which Deserves a Place in Your Portfolio?

In today’s volatile market, investors are searching for ways to diversify their fixed income allocations without sacrificing yield or total return. Two asset classes often considered for this purpose are preferred stocks and high yield bonds. While both offer attractive yields, their risk profiles, tax treatment, and diversification benefits differ in meaningful ways.

What Are Preferred Stocks and High Yield Bonds?

Preferred stocks are hybrid securities, typically issued by companies with strong balance sheets and investment-grade ratings at the senior unsecured level. However, the preferred securities themselves are usually rated as high yield. They offer yields similar to non-investment grade bonds but compensate investors primarily for negative convexity rather than default risk.

Preferred stocks behave like callable bonds, meaning their prices don’t always move favorably when interest rates change. This is called negative convexity: when rates fall, issuers can redeem the shares, capping price gains; when rates rise, prices can drop sharply. Investors earn higher yields not because of high default risk, but as compensation for this call-related price risk.

High yield bonds, on the other hand, are issued by companies with lower credit ratings. Investors in these bonds are compensated mainly for taking on default risk.

Key Differences and Investment Considerations

1. Issuer Quality and Default Risk

Preferred securities are generally issued by companies with higher credit ratings, which can translate to lower default risk compared to high yield bonds. Historical data shows that default rates for preferreds have remained materially below those of high yield bonds, even during periods of market stress such as 2008 and 2023[1].

2. Diversification Benefits

Preferred stocks offer low correlations to both equity markets (S&P 500) and fixed income indices (Bloomberg US Aggregate Bond). Over the past 15 years, preferreds and hybrid securities have also shown very low sensitivity to interest rate changes across the curve. This makes them a powerful tool for diversifying income streams and reducing overall portfolio risk[1].

3. Yield and Tax Treatment

Yields for preferred stocks and high yield bonds are currently similar. However, many preferred securities offer qualified dividend income (QDI), which is taxed at a lower rate than ordinary income. This can make the after-tax yield of preferreds comparable to, or even higher than, high yield bonds for many investors[1].

4. Relative Value and Spreads

Spreads between high yield bonds and preferred securities are relatively tight compared to historical averages. Given the higher quality and diversification benefits of preferreds, this presents an opportunity to allocate at attractive relative values[1].

Risks to Consider

Both preferred stocks and high yield bonds carry risks, including credit risk, interest rate risk, and sector concentration risk. Preferreds also have unique risks such as negative convexity and subordination in the capital structure. It’s important to review fund prospectuses and consult with financial professionals before investing[1].

Conclusion

Preferred stocks and high yield bonds each offer compelling reasons for inclusion in a diversified portfolio. Preferreds stand out for their lower default risk, attractive after-tax yields, and strong diversification benefits. High yield bonds, meanwhile, may offer higher returns in certain market environments but come with greater default risk.

Pairing both asset classes can help investors balance risk and reward, especially in uncertain markets. As always, consider your investment objectives, risk tolerance, and consult with a financial advisor before making allocation decisions.

References

Disclaimers: High yield/junk bonds (grade BB or below) are not investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Asset allocation does not ensure a profit or protect against a loss. (34-LPL)

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. (26-LPL)

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This material was prepared by North Square Investments

Navigating Your 401(k): Why Professional Guidance Matters

Retirement planning has evolved dramatically since the introduction of the 401(k) in 1978. Today, these plans are the cornerstone of retirement savings for millions of Americans, offering flexibility and control—but also placing the responsibility for investment decisions and risk squarely on your shoulders. [CMC6078_1025]

What Makes a 401(k) Special?

- Tax Advantages: You can defer part of your salary into a 401(k), reducing your taxable income now and letting your savings grow tax-deferred until retirement.

- Employer Contributions: Many employers offer matching, profit-sharing, or safe harbor contributions, which can boost your retirement savings. These may follow a vesting schedule, so it pays to understand your plan’s rules.

- Investment Choices: 401(k) plans typically offer a range of investment options, but choosing the right mix can be overwhelming.

Contributions & Withdrawals: Know the Rules

- Pre-tax vs. Roth: Decide whether to contribute pre-tax (pay taxes later) or Roth (pay taxes now, withdraw tax-free in retirement).

- Catch-Up Contributions: If you’re 50 or older, you can contribute extra each year. Starting in 2025, those aged 60–63 can contribute even more.

Early Withdrawals: Taking money out before age 59½ usually means a 10% penalty—unless you qualify for exceptions like the “Rule of 55” or certain hardships.

Rollovers & Special Strategies

- Changing Jobs or Retiring? A plan participant leaving an employer typically has four options (and may engage in a combination of these options), each choice offering advantages and disadvantages.

• 1. Leave the money in former employer’s plan, if permitted; • 2. Roll over the assets to new employer’s plan, if one is available and rollovers are permitted; • 3. Roll over to an IRA; or • 4. Cash out the account value. - Matching Funds to the Right IRA: Pre-tax 401(k) funds go to a traditional IRA; Roth 401(k) funds go to a Roth IRA. Splitting after-tax contributions can optimize your tax benefits.

- Rule of 55: If you leave your job at age 55 or older, you may be able to withdraw from your 401(k) penalty-free.

- Net Unrealized Appreciation (NUA): Special tax treatment for employer stock can save you money if handled correctly.

Why Work with a Wealth Advisor?

The rules around 401(k)s, rollovers, and retirement planning are complex. A wealth advisor can help you:

- Customize Your Strategy: Tailor your plan to your unique goals and circumstances.

- Maximize Benefits: Take advantage of options like guaranteed income, downside protection, and charitable giving strategies.

- Stay Compliant: Ensure you meet all legal and fiduciary requirements.

- Optimize Tax Outcomes: Make smart decisions about rollovers and distributions.

The Bottom Line

Your 401(k) is likely one of your largest financial assets. With professional guidance, you can confidently navigate your options, avoid costly mistakes, and optimize your retirement outcomes. Don’t go it alone—partner with a professional to make the most of your retirement journey

Contributions to a Roth IRA are taxed in the contribution year. The Roth IRA offers tax deferral on any earnings in the account. Withdrawals from the account may be tax free, as long as they are considered qualified. Limitations and restrictions may apply. Withdrawals prior to age 59 ½ or prior to the account being opened for 5 years, whichever is later, may result in a 10% IRS penalty tax. Future tax laws can change at any time and may impact the benefits of Roth IRAs. Their tax treatment may change.

FIRST TRUST – Newport Beach

Attendees:

Jeff Baker (First Trust)

Garrett Olson, Smith Capital. Gibson Smith is the founder, CIO

Seve Sakayan of WCM.

We reviewed a few of their products and they gave us an overview of the fixed income and international markets.

Attendees: Dan Romero & Greg Tobey

Location: Pelican Hill

Time: 10:00am (1 Hour)

Estimated Cost: $200

INVESCO – Orange, CA

Met with:

Christopher Collie, CAIA, CIMA®

We reviewed a few of their products and they gave us an overview of the fixed income and momentum trading.

Attendees: Dan Romero & Greg Tobey

Location: El Matatan

Time: 1:15pm

Estimated Cost: $80

EATON VANCE – Orange, CA

Met with

Sam Reinhart, AAMS, CSRIC

We discussed Eaton Vance Equity market perspective, impact of Yields and why they matter, direct indexing and the Eaton Vance Exchange Fund program.

Attendees: Dan Romero & Greg Tobey

Location: Medii Kitchen

Time: 1:15pm

Estimated Cost: $50

Key Tax Policy Differences: House vs. Senate Finance Bills

As lawmakers shape the next chapter of U.S. tax policy, notable differences have emerged between the House and Senate Finance Committee proposals. Financial professionals and investors should be aware of several key distinctions that could influence long-term planning:

1. Trump Accounts

Both chambers support the creation of tax-favored child accounts with a $1,000 government incentive. This shared provision highlights bipartisan support for encouraging early savings and investment among younger Americans.

2. Opportunity Zones

The House bill would eliminate existing Opportunity Zones (OZs) in 2026, while allowing new zones to be designated beginning in 2027. In contrast, the Senate would extend and enhance OZs permanently—indicating a fundamental difference in how each chamber views the long-term utility of these zones.

3. SALT Deduction

A major divergence appears around the State and Local Tax (SALT) deduction. The House proposes a $40,000 deduction for those earning under $500,000, with a phaseout thereafter. The Senate, meanwhile, retains the current $10,000 limit. The House approach would offer broader relief to upper-middle-income households.

4. Qualified Business Income (QBI) Deduction

The House supports a 23% deduction with a stricter phaseout for specified service trades or businesses (SSTBs). The Senate offers a slightly lower 20% deduction but with a more generous $400 baseline and a softer SSTB phase-in. The result: broader access under the Senate plan, higher deduction under the House version.

5. Pass-Through SALT (PTET) Workaround

The House would remove the PTET workaround election for SSTBs, while the Senate keeps the $10,000 SALT cap intact. Both indicate a potential shift away from state-based SALT deduction workarounds for pass-through entities.

6. Bonus Depreciation

The House proposes extending 100% bonus depreciation through 2029, whereas the Senate would make the 100% rate permanent—potentially providing greater certainty for long-term capital investment decisions.

7. Estate, Gift, and GSTT Exemptions

Both bills align here: a $15 million exemption (adjusted for inflation) for estate, gift, and generation-skipping transfer taxes. This consistency provides a level of predictability for estate planners, at least in the near term.

Source: Bob Keebler via the Academy of Preferred Financial Advisors

FORBES RECOGNIZES DAN ROMERO AS A BEST-IN-STATE WEALTH ADVISOR

![]()

[Orange, CA] — [April 2025] – Daniel S. Romero, CFP® an independent LPL Financial advisor in Orange, CA has been recognized in this year’s list of the Forbes/SHOOK Best-in-State Wealth Advisors for his track record of success in the financial services industry. Romero, President of Romero Wealth Mgmt. was recognized as the No. 75 advisor in Southern California.

The annual list is compiled by Forbes with insights from SHOOK Research. Advisors are selected based on quantitative and qualitative data, and are assessed on a variety of criteria, including interviews, years of experience, compliance records and assets under management*.

“We extend our heartfelt congratulations to Dan Romero for the well-deserved recognition from Forbes,” said Julian Lopez, LPL’s executive vice president of Independent Advisor Services Relationship Management. “This award highlights his dedicated efforts in guiding his clients towards financial success, while helping them add inspiration and meaning to their lives and legacies. LPL is steadfast in our support of ambitious advisors like Dan, equipping them with sophisticated investment solutions, advanced technology, and extensive resources to provide unparalleled service and experiences for their clients.”

Daniel S. Romero, CFP® has 29 years of experience in the financial services industry and a full range of financial services for individuals, families and business owners; including retirement and financial planning, individual money management, individual stocks and bonds, alternative investments, mutual funds, annuities and more.

About LPL Financial

LPL Financial Holdings Inc. (Nasdaq: LPLA) is among the fastest growing wealth management firms in the U.S. As a leader in the financial advisor-mediated marketplace, LPL supports nearly 29,000 financial advisors and the wealth management practices of approximately 1,200 financial institutions, servicing and custodying approximately $1.7 trillion in brokerage and advisory assets on behalf of approximately 6 million Americans. The firm provides a wide range of advisor affiliation models, investment solutions, fintech tools and practice management services, ensuring that advisors and institutions have the flexibility to choose the business model, services, and technology resources they need to run thriving businesses. For further information about LPL, please visit www.lpl.com.

Securities and advisory services offered through LPL Financial LLC (“LPL Financial”), a registered investment advisor and broker-dealer, member FINRA/SIPC.

Throughout this communication, the terms “financial advisors” and “advisors” are used to refer to registered representatives and/or investment advisor representatives affiliated with LPL Financial.

We routinely disclose information that may be important to shareholders in the “Investor Relations” or “Press Releases” section of our website.

The Forbes Best-In-State Wealth Advisor ranking, developed by SHOOK Research, is based on in-person and telephone due diligence meetings and a ranking algorithm that includes: client retention, industry experience, review of compliance records, firm nominations; and quantitative criteria, including: assets under management and revenue generated for their firms. Portfolio performance is not a criterion due to varying client objectives and lack of audited data. Neither Forbes nor SHOOK Research receives a fee in exchange for rankings.

Daniel Romero and the financial representatives of Romero Wealth Management are registered with and securities and advisory services offered through LPL Financial, a registered investment advisor, member FINRA/SIPC.

LPL Financial, Forbes, SHOOK Research and Romero Wealth Mgmt. are all separate entities.

This award does not evaluate the quality of services provided to clients and is not indicative of this advisor’s future performance. Neither LPL Financial nor the advisors pay a fee to Forbes in exchange for inclusion in the Best-in-State Wealth Advisors list.

We routinely disclose information that may be important to shareholders in the “Investor Relations“ or “Press Releases“ section of our website.

Market Minute | April 03, 2025

Tariffs, volatility, and what we’re doing about it. Dan Romero shares quick thoughts on the market, what moves we’ve already made, and why we’re staying positioned for what’s next. Watch now for a 60-second market pulse.

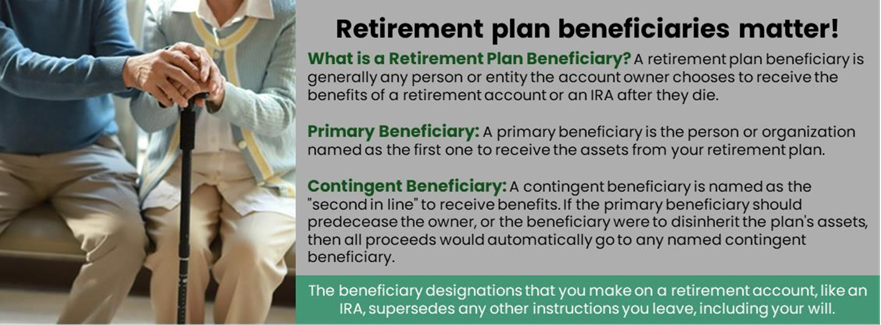

ROTH and Traditional IRAs – Strategies for Building Your Retirement in 2025

Retirement savers understand the importance of being proactive. Having healthy retirement savings can help you live comfortably in your later years. As stewards of our clients’ wealth, we take great satisfaction in helping them prepare for retirement. We also enjoy assisting parents and grandparents who wish to contribute to their loved ones’ futures by properly gifting funds to a retirement account, provided the recipient has earned income and qualifies. Funding retirement accounts at younger ages can significantly improve the chances of enjoying a comfortable financial situation during retirement.

You can contribute to a 2025 IRA until the tax filing deadline of April 15, 2026. The annual contribution limit for 2025 is $7,000, or $8,000 if you are age 50 or older. Your ability to use a Roth IRA contribution can be limited based on your filing status and income (see box in this report). Now is a good time to consider making your 2025 retirement contributions.

For complete rules on Individual Retirement Accounts (IRAs), please visit www.irs.gov Publication 590a or call us to discuss this and all your retirement strategies. In the meantime, here is some information that you may find helpful

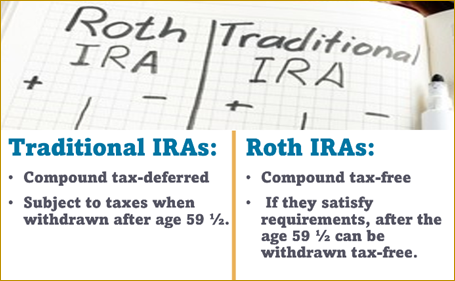

Traditional IRAs

A traditional IRA (Individual Retirement Account) is a way in which individuals can save for retirement and receive tax advantages. Traditional IRAs come in two varieties: deductible and nondeductible. Contributions to a traditional IRA may be fully or partially deductible, depending on your circumstances (i.e., taxpayer’s income, tax-filing status and other factors) and generally, amounts in a traditional IRA (including earnings and gains) are not taxed until distribution.

A clear advantage of traditional IRA accounts is the benefit of deferring taxes on all dividends, interest and capital gains earned inside the IRA account and the potential for annual tax-free compounding. This may allow an IRA to have a faster growth rate than a taxable account.

Roth IRA

A Roth IRA is an IRA that is subject to many of the same rules that apply to a traditional IRA with some major exceptions. Unlike traditional IRAs which can be tax deducted, you cannot deduct contributions to a Roth IRA.

Some Roth IRA advantages include:

- If you satisfy the requirements, qualified distributions can be tax-free.

- You can leave funds in your Roth IRA for your entire lifetime.

- Beneficiaries inherit your Roth IRAs tax-free, if account requirements have been satisfied.

Many investors know and understand that the largest benefit of the Roth IRA is its tax-free withdrawal of contributions, interest and earnings in retirement, but Roth IRAs can also be a powerful part of good estate planning.